Tax-Wise Diversification

Huddleston Law Group, LPA

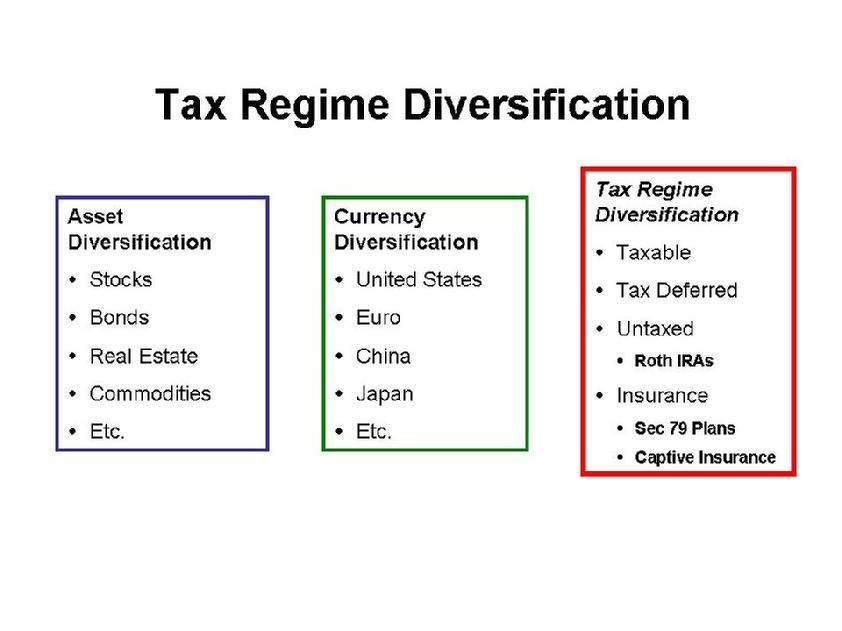

Tax Regime Diversification - Beyond Asset Diversification and Currency Risk Diversification

There is a good chance you have never heard of "Tax Regime Diversification" but you need to understand it because if the U.S. Congress continues on its present path, wealthier Americans will see income taxes skyrocket from their current historically low rates.

You have heard of Asset Diversification and Asset Allocation, because the inventors of modern portfolio theory received a Nobel Prize in Economics for figuring out that Asset Diversification and Allocation is the primary indicator of investment success.

You may have heard of Currency Diversification because of the emergence of new economies and the decline in value of the U.S. dollar. One major international investment firm calculates that 3% (300 basis points) of its overall return comes from currency diversification. Most financial advisors understand currency diversification, although not all of them employ currency diversification strategy in all of their clients' investment plans.

The third wheel of net investment success is what we term Tax Regime Diversification, that is, choosing how to invest among all four income tax regimes in the United States. Very few financial advisors have yet to begin to understand this tool.

The basic premise is simple: Congress taxes our income, although some income is taxed at different rates and some isn't taxed at all. Investments grow better and income is more valuable if it isn't taxed, or at least if it is taxed at lower rates than other investments. So the goal is to understand the various tax regimes and do as much of your investing as possible in no-tax or lower-tax regimes.

Interest on a Certificate of Deposit, for example, is taxed at ordinary income rates. Distributions from your IRA or 401k are taxed at ordinary income rates. Dividends are taxed at capital gains rates, which are lower than ordinary income rates. Personal income, corporate income and trust income can all be taxed at different rates. Some, but not all, of the distributions from annuities are taxed. And on and on.

Distributions from Roth IRAs are not subject to income tax. Neither is income generated inside life insurance policies, which gives insurance companies and insurance policies an advantage over other investors. Congress does this--and so do the tax-writers in other countries--because the insurance industry is so important to the economic safety and security of the citizenry.

Because of profligate spending in Congress, income tax rates are headed much higher for wealthy Americans. They now need--more than ever--investment strategies that will enable them to generate income that is not subject to income tax. Historically, this has been done primarily with tax-free bonds, which are priced to be attractive to top-bracket taxpayers, allowing them to generate returns at least as good as the net after-tax return on taxable investments. But in the emerging income tax environment, better strategies are needed.

It is the goal of this website article to merely to introduce the concept of "tax-regime diversification." If you look at the following, you will see a simplified diagram showing tried and true asset diversification, more recent currency diversification and this new category of tax-regime diversification.

Simply stated, tax regime diversification is the strategy of investing your dollars in more favorably-taxed forms of investment rather than less favorably-taxed forms.

Roth IRAs

You can transmute the income from most classes of assets from taxable to non-taxable by converting a regular IRA or other retirement plan to a Roth IRA. There are no longer any income limits on who can convert from regular to Roth IRAs. As you may know, if you do so, you must pay the prevailing income tax rate at the time of conversion, but thereafter you pay no income tax on the income generated by assets in the Roth IRA, either while they are growing or when you take them out. Software is becoming available that will allow you to see the power of tax-free growth for you, and for your spouse, children and grandchildren.

Life Insurance: Buy Term and Invest the Difference?

There are four reasons that life insurance has started to gain favor as an investment: (1) As we have observed, income tax rates are going up, so the net return on other classes of assets is declining. (2) Until a few years ago, the American insurance industry, in calculating the actuarial likelihood of death, was still using World War II mortality rates, in which millions of Americans died in their teens and twenties. (3) Computerization has had contributed in two ways: It takes far less manpower to do the complex actuarial calculations necessary for an insurance company to prudently price its products, and the accuracy of those calculations is improved. (4) International insurers started competing in the United States.

So, for all intents and purposes, life insurance costs about half as much in 2023 as it did in 2000, even after inflation.

The classic view of life insurance is that it is a bad investment. The historical advice of investment professionals is "Don't use life insurance as an investment. Just buy term insurance and invest the difference." That may no longer be good advice, especially if investment growth in this decade--in which the 10 year growth of the S&P 500 was essentially zero--turns out to be anywhere close to the same as the past decade. There are a few healthy insurance companies whose classic whole life policies are earning 5% in the current economic environment. 5% compounded tax-free over 10 years, however modest such a return might have seemed in recent years, is a very respectable investment return. And in Ohio, the cash value of life insurance is exempt from the claims of creditors.

For Business Owners and Employees: Section 79 Plans

There is a section of the Internal Revenue Code that allows businesses to sponsor insurance plans for their employees, allowing the business to deduct from payroll, and send payments to the insurance companies, for life insurance policies owned by the employees of the business. But when the employee receives his or her W-2, the full amount of the premium is not included. In other words, Section 79 allows the employee to purchase life insurance with partially-pre-tax dollars. The policies in these plans are designed to be paid up quickly, in 5-7 years. And the goal of properly-structured policies in one of these plans is to maximize growth of cash value rather than to maximize the amount of death benefit. Depending on the age and health of the employee, especially the business owner(s), the net after tax value of the cash buildup in a Section 79 insurance policy may be dramatically greater than the value of an IRA or 401K, which are really worth only 30% to 40% of the plan balance after income taxes are considered. If the United States is headed back to the pre-Reagan top marginal rates of more than 70%, the non-taxed 5% return inside an insurance policy purchased partially with pre-tax dollars will likely be far, far superior to ordinary deferred-income retirement accounts. It is the job of your financial advisor and CPA to understand these tools and compare them for you in your individual situation.

For Business Owners: Captive Property and Casualty Insurance Companies

Another method for business owners to put away pre-tax dollars that may or may not ever become subject to income tax--but in any event will be subject only to capital gains tax--is for the business owner to create his or her own "captive" insurance company to insure things that are not currently insured.

By definition, anything a business owner does not insure is "self-insured." We all accept many risks for which we do not purchase property and casualty insurance. But why not insure them if we can afford to pay premiums... to ourselves. The property and casualty insurance premiums paid by a business owner to his captive, or perhaps to a captive owned by his children and/or grandchildren, are fully deductible. The business pays deductible premiums to the captive. The captive must pay its management expenses and its re-insurance premiums. The remaining premium is invested and grows in an income tax free environment. If no claims are paid, the investments continue compounding. (If a claim is paid, the bulk of it is paid by the re-insurer). The pay premiums-and-invest cycle continues year after year. If the money is needed, it is possible for the business owner to borrow from the captive insurer, or someday sell or liquidate the entire company... at capital gains tax rates. After all expenses, the net result is far better than if the business owner paid income taxes and invested in a fully taxable environment.

Many major corporations have formed captive insurance companies, but what has allowed small businesses to take advantage of this section of the tax law is the emergence of "service bureaus" whose business it is to form and operate captive insurance companies for the businesses. It is possible to form captive insurance companies in select states in the United States or in a few select non-U.S. jurisdictions that have "friendlier" insurance laws and lower premium taxes. Any non-U.S. captive should be fully tax-compliant with the United States. The downside of forming an "offshore" captive is the notion that all such companies are tax cheats, a higher compliance and reporting burden and therefore slightly higher costs of formation and maintenance. The choice of jurisdiction, whether or not in the U.S. and what state, or in one of the many favorable foreign jurisdiction, requires a very specialized level of expertise and experience, and varies according to the goals of the business owner and his or her appetite for complexity.

The Takeaway

Taxes of all kinds appear to be headed up. For the foreseeable future, United States government tax policy will be less favorable to individual taxpayers and to the formation and success of business. Taxpaying investors who wish to optimize financial returns and minimize exposure to creditors must now consider not only Asset Diversification and Currency Diversification, but also Tax Regime Diversification, from Roth IRAs to life insurance, and for business owners, those structures and strategies set forth in the Internal Revenue Code that allow thoughtful business owners to reduce their income tax burdens, keeping and protecting more of what they earn.

Copyright Huddleston Law Offices, LPA

Materials may not be reprinted or used without written permission

The subject matter information presented on this website is of a general nature, designed to provide an overview of various subjects, and most of it is not Ohio-specific. The authors, publisher and host are not providing legal, accounting, or specific advice to your situation.

Share On: